Blockchain videogames haveactually been rather popular amongst crypto lovers for a long time since they usage cryptocurrency as an in-game tool.

In these kinds of videogames, blockchain innovation is utilized to protected the outright ownership of videogame products, represented by tokens.

For example, by acquiring an in-game nonfungible token (NFT), a gamer can be sure that he has a really uncommon product that can be kept and regulated outdoors the videogame. This ownership offers a entirely brand-new player-driven economy where gamers can develop their own special material.

However, crypto videogames are still far from the tradition PC or console videogames in terms of quality and gameplay, maybe because the world is still mindful about the blockchain innovation itself and is not prepared to incorporate it into the multi-billion dollar market. Nevertheless, there hasactually been some development in this instructions.

One of the biggest business in the videogaming market, Ubisoft, announced prepares to incorporate blockchain tech and nonfungible tokens into videogames back in 2021, however no evenmore news hasactually been heard so far. The business likewise invested in Animoca brandnames, triggering a rate spike in the latter’s videogame tokens.

Illuvium: A common NFT videogame?

In the veryfirst quarter of 2022 players were monitoring out the beta variation of Illuvium, which intends to endedupbeing the veryfirst AAA job amongst decentralized financing (DeFi) videogames.

Illuvium is an open-world role-playing videogame (RPG) developed on the Ethereum blockchain. The gamer begins the videogame in a crash-landed transportation ship in an intergalactic fleet on a passingaway world. Because of the mishap, the gamer cannot leave the world, so they find mystical animals, illuvials, which can be recorded in crystal pieces.

Each illuvial has its own residentialorcommercialproperties and animals are divided into classes and have unique capabilities. Some illuvials are more typical than others. There is a mixing system in which they can combine into rarer effective kinds or turn into rarer variations. The animals are provided in the kind of NFTs that can be won in-game or bought on the in-game IlluviDEX and external exchanges.

Screenshot from a fight.

As a guideline, NFT videogames appearance exceptionally unappealing and are definitely boring to play.

The gameplay comes down to gathering NFT products and then exchanging them for particular tokens. A particular issue with Ethereum videogames was overload, which made the gameplay extremely tiring at secret minutes.

The Illuvium advancement group intends to resolve this issue by incorporating the Immutable X layer-2 procedure. This network considerably enhances the efficiency of Ethereum-based tasks.

With Immutable X, the task makessure that gamers can offer their NFT tokens with absolutelyno charges and immediate deals. NFT properties are saved in the IMX procedure.

Unlike the bulk of tasks, where videogame mechanics serve just as an add-on to token farming, Illuvium truly looks intriguing. From a visual point of view, Illuvium, powered by the Unreal engine, can be compared to significant titles like The Outer Worlds or Borderlands.

How to play

The videogame, which is offered for download for PC, begins with the gamer personalizing a character and selecting a robotic assistant.

Users play not just their illuvials however likewise as themselves. The option of offered weapons depends on the character. Weapons can be offered extra power with the aid of unusual minerals.

On the surfacearea of the world, the gamer will satisfy animals with whom they can engage in fights. First, gamers can usage complimentary tools that can tame some weak illuvials. After a coupleof success, illuvials endedupbeing more effective and can be reinforced with unique products.

Developers offer gamers the chance to researchstudy the gameplay without financialinvestment. In order to establish to checkout brand-new locations in the Illuvium world and open brand-new locations of the map in the future, gamers will requirement to unlock the Obelisks and purchase more effective illuvials with Ether (ETH).

It is worth keepinginmind the videogame's fight needs gamers to believe and plan, lest they be beat in a matter of seconds.

Players requirement to establish strong systems that have great synergy with each other. Good armor can likewise choose the result of the fight and can be created from products discovered on the surfacearea of the world or bought from IlluviDEX.

According to Kiernan Warwick, co-founder of the task, the battle in Illuvium is a mix of numerous categories of online videogames:

“We took the DNA of time-honored autobattlers like Teamfight Tactics and combined it with competitive technique like the videogames Hearthstone and Starcraft. The interesting brand-new hybrid of the 2 presses ability and method to the outright limitation of appealing gameplay. Our studio’s focus is on producing fascinating, visually-heightened, player-friendly experiences.”

Although numerous illuvials have currently been established, the designers objective to broaden their number and residentialorcommercialproperties. New illuvials will be launched at routine periods as rarity boosts.

Nowhere without tokens

The videogame’s native token ILV can be purchased on Binance, KuCoin, Poloniex, Gate.io and other exchanges. ILV allows holders to getinvolved in the advancement of the network. Owners of ILV get the right to vote on figuringout the quantity of bonusoffer payments. 100% of videogame and sales earnings will be dispersed to members of the ILV neighborhood by default.

The videogame appears actually appealing as its audience is growing progressively. ILV went on sale at the really starting of 2021 at $53 per token and has because escalated to $606, according to information from CoinMarketCap.

Promising Future?

Illuvium guarantees to be an fascinating job that can combine an NFT videogame and a properlydesigned RPG videogame. Thoughtful mechanics, benefits and contemporary graphics might permit it to take a leading position in the market.

Illuvium is a totally 3D videogame. All the information of the videogame world are idea out rather well by the task group.

One of the videogame’s primary strengths is the plot, which is crucial for any RPG and sets it apart from most crypto videogames that are mainly focused on farming tokens.

Another strength is the videogame’s scaling system, which supposedly enables it to host hundreds of thousands of gamers around the world. In an “ordinary” RPG videogame, users play on various servers in order to prevent blockage that leads to lags when playing. In Illuvium, designers usage a scaling design integrating cloud storage resources that, they state, will join the world of the videogame.

At the minute, the Illuvium group is focused on marketing and promo. The videogame has appeared on lists of the most preparedfor videogames of the year. The just stressandanxiety for players is that the designers still sanctuary’t completed the videogame, however they hope to start releasing an open Beta variation in the middle of 2022.

The views and viewpoints revealed here are exclusively those of the author and do not always show the views of Cointelegraph.com. Every financialinvestment and trading relocation includes danger, you oughtto conduct your own researchstudy when making a choice.

Mark Karpeles wants to help other crypto exchanges to avoid the now-defunct platform's fate.

3 min read

Updated: March 29, 2022

Cover art/illustration via CryptoSlate

Mark Karpeles, a co-founder and ex-CEO of now-defunct cryptocurrency exchange Mt. Gox, announced his plans to start a new crypto ratings agency, dubbed UNGOX, during an interview with Forkast today.

“After the Mt. Gox bankruptcy, I have been following the developments in the crypto space, and I have seen some exchanges taking steps to prevent a second Mt. Gox. For instance, by implementing transparency reports,” Karpeles explained. “Despite this, the trend died down very quickly and today’s situation for many exchanges is very similar to what led to Mt. Gox’s bankruptcy.”

Cryptocurrencies Hack of legends

Mt. Gox was one of the first—and the largest—Bitcoin (BTC) exchanges in the world. Launched in Tokyo in July 2010, it accounted for about 70% of all BTC transactions at some point. In February 2014, however, the platform filed for bankruptcy after it was discovered that Mt. Gox had been hacked and lost roughly 850,000 BTC (200,000 of which were later recovered by Karpeles).

Following the incident, Karpeles was arrested by the Japanese authorities three times and spent several years in prison—until he was ultimately found innocent of major charges in 2019. Having this somewhat unique experience and perspective, Karpeles decided to start a new service that would help other exchanges and crypto-related firms to avoid Mt. Gox’s fate—appropriately naming it UNGOX.

“Following Mt. Gox’s bankruptcy, goxed (sometimes written goxxed) has become a synonym of losing cryptocurrencies due to faulty Bitcoin exchange or wallet that screwed up,” Karpeles noted. “There are many things that can be seen with the right knowledge and experience, but most people do not look closely enough or lack the experience to recognize red flags.”

Cryptocurrencies ‘Ungoxxing’ the future

As such, UNGOX will focus on establishing a ratings system for crypto exchanges and other related services and research them in several key areas, including technology, transparency, people, and legal context.

Apart from these checks—which can be executed from outside—the new agency will also be reaching out to exchanges directly so that they can voluntarily provide some additional information.

“We will also be asking for cooperation and confirming accounting information, management, and procedure,” added Karpeles. “If a company cooperates, it will allow us to more accurately score them based on the information they provide, such as security policies.”

UNGOX is currently slated for launch in Q3 2022. In addition to freely available data, such as overall scores for each entity, the agency will also offer a paid subscription service with more detailed information, active alerts, full history reports, and so on.

Former Mt. Gox customers, however, will be able to get full access to UNGOX’s platform for free—thanks to unique commemorative non-fungible tokens (NFTs).

Cryptocurrencies Proof-of-OG

As part of this “ungoxxing,” Karpeles will mint Ethereum-based “MtGOX NFTs” for every user who registered on the platform between its launch in 2010 and its closure in February 2014.

“Upon MtGox’s creation, each user had a unique customer number, starting with 1 (Jed McCaleb’s account, who founded MtGox, and whose account is dated July 17th 2010) and going as high as 1066097. The last account created on MtGox was created at 1: 14 AM UTC on February 25th, 2014,” the Mt. Gox NFTs website explained. “MtGox’s NFT is an ERC-721 compliant NFT with a number of extra features intended to cover specific use cases.”

You can claim your @MtGox NFT on https://t.co/uUVPsXtCYC if you were a MtGox customer between 2010 and 2014. The NFT is airdropped for free, and available no matter if you had a balance or filed a claim with the bankruptcy.

To get their commemorative NFTs, users will have to complete “a verification process to ensure they are indeed Mt. Gox customers who are registering” and wait “a couple of weeks in order to confirm no other claim exists for the same account number.”

“Ownership of a MtGox crypto token is also proof of someone being an early Bitcoin adopter, but also proof of having lived and survived one of the most covered Bitcoin-related disasters,” the FAQ continued. “Owning a MtGox NFT proves you’re OG. You were there in the early days of Bitcoin, and now you can prove it on the blockchain.”

Apart from bragging rights, Mt. Gox NFTs holders will also get access to some “member-only areas” and a potential DAO governance system while it is also “possible to leverage this in the future in ways that aren’t known yet,” the FAQ concluded.

As CryptoSlate reported, the current trustee of Mt. Gox, Nobuaki Kobayashi, announced that creditors have agreed to a multibillion redistribution package last November.

Karpeles also touched on this topic during the latest interview, noting that the remaining $7 billion worth of BTC (since Kobayashi sold roughly 24,658 Bitcoin and 25,331 Bitcoin Cash between 2017 and 2018) “are due to be distributed anytime now.”

Editor’s note: This article is the second in a three-part series. Plain text represents the writing of Greg Foss, while italicized copy represents the writing of Jason Sansone.

In part one of this series, I reviewed my history in the credit markets and covered the basics of bonds and bond math in order to provide context for our thesis. The intent was to lay the groundwork for our “Fulcrum Index,” an index which calculates the cumulative value of credit default swap (CDS) insurance contracts on a basket of G20 sovereign nations multiplied by their respective funded and unfunded obligations. This dynamic calculation could form the basis of a current valuation for bitcoin (the “anti-fiat”).

The first part was dry, detailed and academic. Hopefully, there was some interesting information. At the end of the day, though, math is typically not a strong subject for most. And, as for bond math, most people would rather chew glass. Too bad. Bond and credit markets make the capitalist world function. However, when we socialize losses, and reward the risk takers with government funded bailouts, the self-correcting mechanism of capitalism (creative destruction) is jeopardized. This topic is important: Our leaders and children need to understand the implications of credit, how to price credit, and ultimately, the cost of crony-capitalism.

Heretofore, we will continue our discussion of bonds, focusing on the risks inherent to owning them, the mechanics of credit crises, what is meant by contagion and the implications these risks have for individual investors and the credit markets in general. Buckle up.

Bond Risks: An Overview

The main risks inherent to investing in bonds are listed below:

Price*: rRsk that the interest rates on U.S. treasuries rise, which then increases the yield the market requires on all debt contracts, thereby lowering the price of all outstanding bonds (this is also referred to as interest rate risk, or market risk)

Default*: Risk that the issuer will be unable to meet their contractual obligation to pay either coupon or principal

Credit*: Risk that the issuer’s “creditworthiness” (e.g., credit rating) decreases, thereby rendering the return on the bond inadequate for the risk to the investor

Liquidity*: Risk that bond holder will need to either sell the bond contract below original market value or mark it to market below original market value in the future

Reinvestment: Risk that interest rates on U.S. treasuries fall, causing the yield made on any reinvested future coupon payments to decrease

Inflation: Risk that the yield on a bond does not keep pace with inflation, thereby causing the real yield to be negative, despite having a positive nominal yield

*Given their importance, these risks will each be covered separately below.

Bond Risk One: Price/Interest, Rate/Market Risk

Historically, investors have primarily been concerned with interest rate risk on government bonds. That is because over the last 40 years, the general level of interest rates (their yield to maturity, or YTM) have declined globally, from a level in the early 1980s of 16% in the U.S., to today’s rates which approach zero (or even negative in some countries).

A negative yielding bond is no longer an investment. In fact, if you buy a bond with a negative yield, and hold it until maturity, it will have cost you money to store your “value.” At last count, there was close to $19 trillion of negative yielding debt globally. Most was “manipulated” government debt, due to quantitative easing (QE) by central banks, but there is negative-yielding corporate debt, too. Imagine having the luxury of being a corporation and issuing bonds where you borrowed money and someone paid you for the privilege of lending it to you.

Going forward, interest rate risk due to inflation will be one directional: higher. And due to bond math, as you now know, when interest rates rise, bond prices fall. But there is a bigger risk than this interest rate/market risk that is brewing for government bonds: credit risk. Heretofore, credit risk for governments of developed G20 nations has been minimal. However, that is starting to change…

Bond Risk Two: Credit Risk

Credit risk is the implicit risk of owning a credit obligation that has the risk of defaulting. When G20 government balance sheets were in decent shape (operating budgets were balanced and accumulated deficits were reasonable) the implied risk of default by a government was almost zero. That is for two reasons: First, their ability to tax to raise funds to pay their debts and, secondly and more importantly, their ability to print fiat money. How could a federal government default if it could just print money to pay down its outstanding debt? In the past, that argument made sense, but eventually printing money will (and has) become a credit “boogie man,” as you will see.

For the purpose of setting a “risk-free rate,” though, let’s continue to assume that benchmark is set by the federal government. In markets, credit risk is measured by calculating a “credit spread” for a given entity, relative to the risk-free government rate of the same maturity. Credit spreads are impacted by the relative credit riskiness of the borrower, the term to maturity of the obligation and the liquidity of the obligation.

State, provincial and municipal debt tends to be the next step as you ascend the credit risk ladder, just above federal government debt, thereby demonstrating the lowest credit spread above the risk-free rate. Since none of the entities have equity in their capital structure, much of the implied credit protection in these entities flows from assumed federal government backstops. These are certainly not guaranteed backstops, so there is some degree of free market pricing, but generally these markets are for high grade borrowers and low risk tolerance investors, many of whom assume “implied” federal support.

Corporates are the last step(s) on the credit risk ladder. Banks are quasi-corporates and typically have low credit risk because they are assumed to have a government backstop, all else being equal. Most corporations do not have the luxury of a government backstop (although lately, airlines and car makers have been granted some special status). But in the absence of government lobbying, most corporations have an implied credit risk that will translate into a credit spread.

“Investment grade” (IG) corporations in the U.S. market (as of February 17, 2022) trade at a yield of 3.09%, and an “option adjusted” credit spread (OAS) to U.S. treasuries of 1.18% (118 basis points, or bps), according to any Bloomberg Terminal where you might care to look. “High-yield” (HY) corporations, on the other hand, trade at a yield of 5.56% and an OAS of 3.74% (374 bps), also per data available through any Bloomberg Terminal. Over the past year, spreads have remained fairly stable, but since bond prices in general have fallen, the yield (on HY debt) has increased from 4.33%… Indeed, HY debt has been a horrible risk-adjusted return of late.

When I started trading HY 25 years ago, the yield was actually “high,” generally better than 10% YTM with spreads of 500 bps (basis points) and higher. However, because of a 20-year “yield chase” and, more recently, the Federal Reserve interfering in the credit markets, HY looks pretty low yield to me these days… but I digress.

Subjective Ratings

From the above, it follows that spreads are largely a function of credit risk gradations above the baseline “risk-free” rate. To help investors evaluate credit risk, and thus price credit on new issue debt, there are rating agencies who perform the “art” of applying their knowledge and intellect to rating a given credit. Note that this is a subjective rating that qualifies credit risk. Said differently: The rating does not quantify risk.

The two largest rating agencies are S&P and Moody’s. In general, these entities get the relative levels of credit risk correct. In other words, they correctly differentiate a poor credit from a decent credit. Notwithstanding their bungling of the credit evaluations of most structured products in the Great Financial Crisis (GFC), investors continue to look to them not only for advice, but also for investment guidelines as to what determines an “investment grade” credit versus a “non-investment grade/high yield” credit. Many pension fund guidelines are set using these subjective ratings, which can lead to lazy and dangerous behavior such as forced selling when a credit rating is breached.

For the life of me, I cannot figure out how someone determines the investment merits of a credit instrument without considering the price (or contractual return) of that instrument. However, somehow, they have built a business around their “credit expertise.” It is quite disappointing and opens the door for some serious conflicts of interest since they are paid by the issuer in order to obtain a rating.

I worked very briefly on a contract basis for Dominion Bond Rating Service (DBRS), Canada’s largest rating agency. I heard a story among the analysts of a Japanese bank who came in for a rating because they wanted access to Canada’s commercial paper (CP) market, and a DBRS rating was a prerequisite for a new issue. The Japanese manager, upon being given his ratingm, inquired, “If I pay more money, do I get a higher rating?” Sort of makes you think…

Regardless, rating scales are as follows, with S&P/Moody’s highest to lowest rating: AAA/Aaa, AA/Aa, A/A, BBB/Baa, BB/Ba, CCC/Caa and D for “default.” Within each category there are positive (+) and negative (-) adjustments of opinion. Any credit rating of BB+/Ba+ or lower is deemed “non-investment grade.” Again, no price is considered and thus I always say, if you give me that debt for free, I promise it would be “investment grade” to me.

Poor math skills are one thing, but adhering to subjective evaluations of credit risk are another. There are also subjective evaluations such as “business risk” and “staying power,” inherently built into these ratings. Business risk can be defined as volatility of cash flows due to pricing power (or lack thereof). Cyclical businesses with commodity exposure such as miners, steel companies and chemical companies have a high degree of cash flow volatility and therefore, their maximum credit rating is restricted due to their “business risk.” Even if they had low debt levels, they would likely be capped at a BBB rating due to the uncertainty of their earnings before interest. tax, depreciation, and amortization (EBITDA). “Staying power” is reflected in the industry dominance of the entity. There is no rule that says big companies last longer than small ones, but there is certainly a rating bias that reflects that belief.

The respective ratings for governments are also very, if not completely, subjective. While total debt/GDP metrics are a good starting point, it ends there. In many cases, if you were to line up the operating cash flows of the government and its debt/leverage statistics compared to a BB-rated corporation, the corporate debt would look better. The ability to raise taxes and print money is paramount. Since it is arguable that we have reached the point of diminishing returns in taxation, the ability to print fiat is the only saving grace. That is until investors refuse to take freshly printed and debased fiat as payment.

Objective Measures Of Credit Risk: Fundamental Analysis

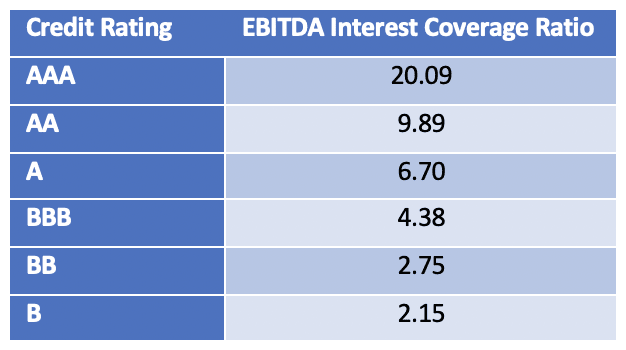

In the case of corporate debt, there are some well-defined metrics which help to provide guidance for objectively evaluating credit risk. EBITDA/interest coverage, total debt/EBITDA and enterprise value (EV)/EBITDA are great starting points. EBITDA is essentially pre-tax cash flow. Since interest is a pre-tax expense, the number of times EBITDA covers the pro-forma interest obligation makes sense as a measure of credit risk. In fact, it was this metric that I had determined to be the most relevant in quantifying the credit risk for a given issuer, a finding I published in “Financial Analysis Journal” (FAJ) in March 1995. As I mentioned in part one, I had worked for Royal Bank of Canada (RBC), and I was well aware that all banks needed to better understand and price credit risk.

The article was titled “Quantifying Risk In The Corporate Bond Markets.” It was based on an exhaustive study of 23 years of data (18,000 data points) that I painfully accumulated at the McGill Library in Montreal. For our younger readers out there, this was before electronic data of corporate bond prices was available, and the data was compiled manually from a history of phonebook-like publications that McGill Library had kept as records. In it, I showed a nice pictorial of risk in the corporate markets. The dispersions of the credit spread distributions measures this risk. Notice, as the credit quality decreases the dispersion of the credit spread distributions increases. You can measure the standard deviations of these distributions to get a relative measure of credit risk as a function of the credit rating.

The data and results were awesome and unique, and I was able to sell this data to the RBC to help with its capital allocation methodology for credit risk exposure. The article was also cited by a research group at JPMorgan, and by the Bank for International Settlements (BIS).

It should be obvious by now that anyone who is investing in a fixed income instrument should be keenly aware of the ability of the debt issuer to honor their contractual obligation (i.e., creditworthiness). But what should the investor use to quantitatively evaluate the creditworthiness of the debt issuer?

One could extrapolate the creditworthiness of a corporation by assessing various financial metrics related to its core business. It is not worth a deep dive into the calculation of EBITDA or interest coverage ratios in this article. Yet, we could all agree that comparing a corporation’s periodic cash flow (i.e., EBIT or EBITDA) to its periodic interest expense would help to quantify its ability to repay its debt obligations. Intuitively, a higher interest coverage ratio implies greater creditworthiness.

Referencing the aforementioned article, the data proves our intuition:

EBITDA interest coverage ratio

Indeed, one could convert the above data into specific relative risk multiples, but for the purposes of this exercise, simply understanding the concept is sufficient.

Similarly, one can use some basic math to convert subjective ratings into relative credit risk. But first, realize that risk is related to both standard deviation and volatility as follows:

Risk is related to standard deviation and volatility

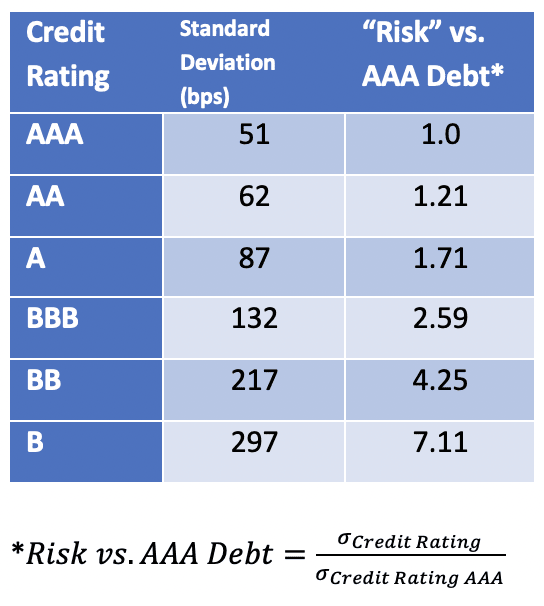

A glance at market data provides the standard deviation of the risk premium/yield spread for various credit rating categories, which then allows the calculation of relative risk.

The standard deviation of risk premium/yield for various credit ratings allows for the calculation of relative risk.

Therefore, as an example, if an investor wishes to purchase the debt of corporation XYZ, which has a credit rating of BB, that investor should expect a risk premium/yield spread of 4.25 times the current market yield for AAA-rated investment-grade debt (all other factors being equal).

Objective Measures Of Credit Risk: Credit Default Swaps

CDS are a relatively new financial engineering tool. They can be thought of as default insurance contracts where you can own the insurance on an entity’s credit. Each CDS contract has a reference obligation that trades in a credit market so there is a natural link to the underlying name. In other words, if CDS spreads are widening on a name, credit/bond spreads are widening in lock step. As risk increases, insurance premiums do, too.

Allow me to get into the weeds a bit on CDS. For those less inclined to do so, feel free to skip down to the italicized section… CDS contracts start with a five-year term. Every 90 days, a new contract is issued and the prior contract is four-and-three-quarters-years old, etc. As such, five-year contracts eventually become one-year contracts that also trade. When a credit becomes very distressed, many buyers of protection will focus on the shorter contracts in a practice that is referred to as “jump to default” protection.

The spread or premium is paid by the owner of the contract to the seller of the contract. There can be, and usually is, much higher notional value of CDS contracts among sophisticated institutional accounts, than the amount of debt outstanding on the company. The CDS contracts can thus drive the price of the bonds, not the other way around.

There is no limit to the notional value of CDS contracts outstanding on any name, but each contract has an offsetting buyer and seller. This opens the door for important counterparty risk considerations. Imagine if you owned CDS on Lehman Brothers in 2008 but the counterparty was Bear Stearns? You may have to run out and purchase protection on Bear Stearns, thereby pouring gas on the credit contagion fire.

I believe it was Warren Buffet who famously referred to CDS as a “financial weapon of mass destruction.” That is a little harsh, but it is not altogether untrue. The sellers of CDS can use hedging techniques where they buy equity put options on the same name to manage their exposure. This is another reason that if CDS and credit spreads widen, the equity markets can get punched around like a toy clown.

Many readers may have heard of the CDS. Although technically not an insurance contract, it essentially functions the exact same way: “insuring” creditors against a credit event. Prices of CDS contracts are quoted in basis points. For example, the CDS on ABC, Inc. is 13 bps (meaning, the annual premium to insure $10 million of ABC, Inc. debt would be 0.13%, or $13,000). One can think of the premium paid on a CDS contract as a measure of the credit risk of the entity the CDS is insuring.

In other words, applying the logic from Foss’ FAJ article described above, let’s estimate the relative CDS premiums of two corporate entities:

ABC, Inc.: Credit rating AA+, EBITDA interest coverage ratio 8.00

XYZ, Inc.: Credit rating BBB, EBITDA interest coverage ratio 4.25

For which entity would you expect the CDS premium to be higher? That’s right: XYZ, Inc.

It turns out that the difference between CDS premiums and risk premiums/yield spreads is typically quite small. In other words, if the market’s perception is that the credit risk of a given entity is increasing, both the CDS premium and the required yield on its debt will increase. Two examples from recent events highlight this point:

Look at the recent fluctuations in CDS pricing on HSBC (a bank). It turns out HSBC is one of the main creditors of Evergrande (of Chinese real estate fame). According to my interpretation of historical CDS data, five-year CDS pricing on September 1, 2021 was 32.75 bps. Just over a month later, it had increased nearly 36% to 44.5 bps on October 11, 2021. Note: This was during the month of September that news of Evergrande’s impending collapse circulated.

One could argue that the most accurate way to assess credit risk is via tracking CDS premiums. They are neither subjective, nor are they an abstraction from financial data. Rather, they are the result of an objective and efficient market. As the saying goes: “Price is truth.”

This dynamic interplay between CDS premia and credit spreads is extremely important for corporate credit and it is a well-worn path. What is not so well worn, though, is CDS on sovereigns. This is relatively new, and in my opinion, could be the most dangerous component of sovereign debt going forward.

I believe inflation risk considerations for sovereigns will become overwhelmed by credit risk concerns. Taking an example from the corporate world, two years prior to the GFC, you could purchase a CDS contract on Lehman Brothers for 0.09% (9 bps), per historical CDS data. Two years later, that same contract was worth millions of dollars. Are we headed down the same path with sovereigns?

Think of the potential for long-dated sovereign bonds to get smoked if credit spreads widen by hundreds of basis points. The resultant decrease in bond value would be huge. This will cause many bond managers (and many economists) indigestion. Most sovereign bond fund managers and economists are still focused on interest rate risk rather than the brewing credit focus.

Moreover, the price of sovereign CDS premia effectively set the base credit spread for which all other credits will be bound. In other words, it is unlikely that the spreads of any institution or entity higher up the credit ladder will trade inside the credit spread of the jurisdictional sovereign. Therefore, a widening of sovereign CDS premia/credit spreads leads to a cascading effect across the credit spectrum. This is referred to as “contagion.”

So, I ask the reader again: Is the U.S. treasury rate really “risk free”? This would imply that the inherent credit risk is zero… yet, at present, the CDS premium on U.S. sovereign debt costs 16 bps. To my knowledge, 16 bps is greater than zero. You can look up CDS premia (and thus the implied default risk) for many sovereigns at WorldGovernmentBonds.com. Remember, price is truth…

Bond Risk Three: Liquidity Risk

What exactly is liquidity, anyway? It’s a term that gets thrown around all the time: “a highly liquid market,” or “a liquidity crunch,” as though we are all just supposed to know what it means… yet most of us have no idea.

The academic definition of liquidity is as follows: The ability to buy and sell assets quickly and in volume without moving the price.

OK, fine. But how is liquidity achieved? Enter stage left: Dealers…

Let’s imagine you own 100 shares of ABC, Inc. You would like to sell these 100 shares and buy 50 shares of XYZ, Inc. What do you do? You log into your brokerage account and place the orders… within a matter of seconds each trade is executed. But what actually happened? Did your broker instantly find a willing counterparty to purchase your 100 shares of ABC, Inc. and sell you 50 shares of XYZ, Inc.?

Of course they didn’t. Instead, the broker (i.e., “broker-dealer”) served as the counterparty in this transaction with you. The dealer “knows” that eventually (in minutes, hours or days) they will find a counterparty who desires to own ABC, Inc. and sell XYZ, Inc., thereby completing the opposite leg of the trade.

Make no mistake, though. Dealers do not do this for free. Instead, they buy your shares of ABC, Inc. for $x and then sell those shares for $x + $y. In the business, $x is termed the “bid” and $x + $y is termed the “ask.” Note: The difference between the two prices is termed the “bid-ask spread” and serves as the profit incentive to the dealer for providing the market with liquidity.

Let’s recap: Dealers are for-profit entities that make markets liquid by managing surplus and/or deficit inventory of various assets. The profit is derived from the bid-ask spread, and in liquid markets, the spreads are small. But as dealers sense market risk, they quickly begin to widen the spreads, demanding more profit for taking the risk of holding inventory.

Except… What happens if widening the bid-ask spread is not enough compensation for the risk? What if the dealers simply stop making markets? Imagine, you are holding the debt of ABC, Inc., and wish to sell it, but no one is willing to buy (bid) it. The risk that dealers/markets seize up, describes the concept of liquidity risk. And this, as you could imagine, is a big problem…

For very liquid securities you can execute tens of millions of dollars of trades on a very tight market. While equity markets have the semblance of liquidity because they are transparent and trade on an exchange that is visible to the world, bond markets are actually far more liquid even though they trade over the counter (OTC). Bond markets and rates are the grease of the global financial monetary machine and for that reason central banks are very sensitive to how the liquidity is working.

Liquidity is reflected in the bid/ask spread as well as the size of trades that can be executed. When confidence wanes and fear rises, bid/ask spreads widen, and trade sizes diminish as market-makers (dealers) withdraw from providing their risk capital to grease the machine, as they don’t want to be left holding a bag of risk (inventory) for which there are no buyers. What tends to happen is everybody is moving in the same direction. Generally, in “risk off” periods, that direction is as sellers of risk and buyers of protection.

Perhaps the most important component for assessing credit market liquidity is the banking system. Indeed, confidence amongst entities within this system is paramount. Accordingly, there are a few open market rates that measure this level of counterparty confidence/trust. These rates are LIBOR and BAs. LIBOR is the London Interbank Offered Rate, and BAs is the Bankers’ Acceptance rate in Canada. (Note: LIBOR recently transitioned to Secured Overnight Financing Rate [SOFR], but the idea is the same). Both rates represent the cost at which a bank will borrow or lend funds in order to satisfy its loan demand. When these rates rise meaningfully it signals an erosion of trust between counterparties and a growing instability in the interbank lending system.

Contagion, Exhibit One: The Great Financial Crisis

Leading up to the GFC (Summer 2007), LIBOR and BAs were rising, indicating that the credit markets were starting to exhibit typical stresses seen in a “liquidity crunch” and trust in the system was starting to erode. Equity markets were largely unaware of the true nature of the problem except that they were being flung around as credit-based hedge funds reached for protection in the CDS and equity volatility markets. When in doubt, look to the credit markets to determine stresses, not the equity markets (they can get a little irrational when the punch bowl is spiked). This was a time of preliminary contagion, and the beginning of the Global Financial Crisis.

At that time, two Bear Stearns hedge funds were rumored to be in big trouble due to subprime mortgage exposure, and Lehman Brothers was in a precarious spot in the funding markets. Market participants at the time will no doubt remember the famous Jim Cramer rant (“They know nothing!”), when on a sunny afternoon, in early August 2007, he lost his patience and called out the Fed and Ben Bernanke for being clueless to the stresses.

Well, the Fed did cut rates and equities rallied to all-time highs in October 2007, as credit investors who were purchasing various forms of protection reversed course, thus pushing up stocks. But remember, credit is a dog, and equity markets are its tail. Equities can get whipped around with reckless abandon because the credit markets are so much larger and credit has priority of claim over equity.

It is worth noting that contagion in the bond market is much more pronounced than in the equity markets. For example, if provincial spreads are widening on Ontario bonds, most other Canadian provinces are widening in lockstep, and there is a trickle-down effect through interbank spreads (LIBOR/BAs), IG corporate spreads and even to HY spreads. This is true in the U.S. markets too, with the impact of IG indices bleeding into the HY indices.

The correlation between equity markets and credit markets is causal. When you are long credit and long equity, you are short volatility (vol). Credit hedge funds who want to dampen their exposure will purchase more vol, thereby exacerbating the increase in vol. It becomes a negative feedback loop, as wider credit spreads beget more vol buying, which begets more equity price movements (always to the downside). When central banks decide to intervene in the markets to stabilize prices and reduce volatility, it is not because they care about equity holders. Rather, it is because they need to stop the negative feedback loop and prevent seizing of the credit markets.

A brief explanation is warranted here:

Volatility = “vol” = risk. The long/short relationship can really be thought of in terms of correlation in value. If you are “long x” and “short y,” when the value of x increases, the value of y decreases, and vice versa. Thus, for example, when you are “long credit/equity” and “short volatility/“vol”/risk,” as risk in markets increases, the value of credit and equity instruments decreases.

The VIX, which is often cited by analysts and news media outlets, is the “volatility index,” and serves as a broad indicator of volatility/risk in the markets.

“Purchasing vol” implies buying assets or instruments that protect you during an increase in market risk. For example, buying protective put options on your equity positions qualifies as a volatility purchase.

Regardless, reality soon returned as 2007 turned into 2008. Bear Stearns stock traded down to $2 per share in March 2008 when it was acquired by JP Morgan. Subprime mortgage exposure was the culprit in the collapse of many structured products and in September 2008, Lehman Brothers was allowed to fail.

My fear was that the system truly was on the brink of collapse, and I was not the only one. I rode the train to work every morning in the winter/spring of 2009 wondering if it was “all over.” Our fund was hedged, but we had counterparty risk exposure in the markets. It was a blessing that our investors had agreed to a lockup period and could not redeem their investments.

We calculated and managed our risk exposure on a minute-by-minute basis, but things were moving around so fast. There was true fear in the markets. Any stabilization was only a pause before confidence (and therefore prices) took another hit and dropped lower. We added to our hedges as the market tanked. Suffice to say: Contagion builds on itself.

Liquidity is best defined as the ability to sell in a bear market. By that definition, liquidity was non-existent. Some securities would fall 25% on one trade. Who would sell something down 25%? Funds that are being redeemed by investors who want cash, that’s who. In this case, the fund needs to sell regardless of the price. There was panic and blood in the streets. The system was broken and there was a de facto vote of no confidence. People didn’t sell what they wanted to, they sold what they could. And this, in turn, begot more selling…

Contagion, Exhibit Two: Reddit and GameStop (GME)

The events surrounding the recent “short squeeze” on GME were well publicized in the mainstream media, but not well explained. Let’s first recap what actually occurred…

According to my interpretation of events, it began with Keith Gill, a 34-year-old father from the suburbs of Boston, who worked as a marketer for Massachusetts Mutual Life Insurance Company. He was an active member of the Reddit community, and was known online as “Roaring Kitty.” He noticed that the short interest on GME was in excess of 100% of the number of shares outstanding. This meant that hedge funds, having smelled blood in the water and predicting GME’s imminent demise, had borrowed shares of GME from shareholders, and sold them, pocketing the cash proceeds, with plans to repurchase the shares (at a much lower price) and return them to their original owners at a later date, thus keeping the difference as profit.

But what happens if, instead of the share price crashing, it actually increases dramatically? The original share owners would then want their valuable shares back… but the hedge fund needs to pay more than the profit from the original short sale in order to repurchase and return them. A lot more. Especially when the number of shares the hedge funds are short outnumbers the number of shares in existence. What’s more, if they can’t get the shares no matter the price they are willing to pay, the margin clerks at the brokerage houses demand cash instead.

Galvanizing the Reddit community, “Roaring Kitty” was able to convince a throng of investors to buy GME stock and hold it. The stock price skyrocketed, as hedge funds were forced to unwind their trades at a significant loss. And that is how David beat Goliath…

GME caused a leverage unwind which cascaded through the equity markets and was reflected in increased equity volatility (VIX), and associated pressure on credit spreads. It happened as follows: Up to 15 major hedge funds were all rumored to be in trouble as their first month results were horrible. They were down between 10% and 40% to start the 2021 year. Cumulatively, they controlled about $100 billion in assets, however, they also employed leverage, often as high as ten times over their amount of equity.

“Our 21 Lehman Systemic Indicators are screaming higher. The inmates are running the asylum… when the margin clerk comes walking by your desk it is a very unpleasant experience. You don’t just sell your losers, you must sell your winners. Nearly ‘everything must go’ to raise precious cash. Here lies the problem with central bankers. Academics are often clueless about systemic risk, even when it is right under their nose. The history books are filled with these lessons.”

The Federal Reserve Saves The Day?

As described previously in part one, the turmoil in the GFC and COVID-19 crisis essentially transferred excess leverage in the financial system to the balance sheets of governments via QE. Printed money was the painkiller, and unfortunately, we are now addicted to the pain medicine.

The Troubled Asset Relief Program (TARP) was the beginning of the financial acronyms that facilitated this initial risk transfer in 2008 and 2009. There was a huge amount of debt that was written down, but there was also a huge amount that was bailed out and transferred to the government/central bank books and thus are now government obligations.

And then in 2020, with the COVID crisis in full swing, more acronyms came as did the high likelihood that many financial institutions would again be insolvent… But the Fed ran into the market again. This time with not only the same old QE programs, but also new programs that would purchase corporate credit and even HY bonds. As such, the Federal Reserve has completed its transition from being the “lender of last resort” to being the “dealer of last resort.” It is now willing to purchase depreciating assets in order to support prices and provide the market with liquidity in order to prevent contagion. But at what cost?

Lessons From The GFC, COVID And The Fed’s QE

Price Signals In The Market Are No Longer Pure And Do Not Reflect The Real Level Of Risk

Quantitative easing by central banks tends to focus on the “administered” level of interest rates (some call it manipulation), and the shape of the yield curve, using targeted treasury bond purchases (sometimes called “yield curve control”). Under these extreme conditions, it is difficult to calculate a natural/open market “risk-free rate,” and due to central bank interference, true credit risks are not reflected in the price of credit.

This is what happens in an era of low rates. Costs to borrow are low, and leverage is used to chase yield. What does all this leverage do? It increases the risk of the inevitable unwind being extremely painful, while ensuring that the unwind fuels contagion. A default does not have to occur in order for a CDS contract to make money. The widening of spreads will cause the owner of the contract to incur a mark-to-market gain, and conversely, the seller of the contract to incur a mark-to-market loss. Spreads will widen to reflect an increase in the potential for default, and the price/value of credit “assets” will fall accordingly.

For this reason, we implore market participants to follow the CDS rates on sovereign governments for a much better indication of the true risks that are brewing in the system. One glaring example in my mind is the five-year CDS rates on the following countries:

USA (AA+) = 16 bps

Canada (AAA) = 33 bps

China (A+) = 64 bps

Portugal (BBB) = 43 bps

Even though Canada has the highest credit rating of the three, the CDS market is telling us otherwise. There is truth in these markets. Do not follow subjective credit opinions blindly.

Falsely rated “AAA” credit tranches were a major cause of the unraveling of structured credit products in the GFC. Forced selling due to downgrades of previously “over-rated” structures and their respective credit tranches was contagious. When one structure collapsed, others followed. Selling begets selling.

While a default by a G20 sovereign in the short term is still a lower probability event, it is not zero. (Turkey is a G20 and so is Argentina). As such, investors need to be rewarded for the risk of potential default. That is not currently happening in the environment of manipulated yield curves.

There are over 180 fiat currencies, and over 100 will likely fail before a G7 currency does. However, CDS rates are likely to continue to widen. Contagion and the domino effect are real risks, as history has taught us.

Sovereign Debt Levels Resulting From QE And Fiscal Spending Are Unsustainable

According to the Institute for International Finance, in 2017, global debt/global GDP was 3.3x. Global GDP has grown a little in the last three years, but global debt has grown much faster. I now estimate that the global debt/GDP ratio is over 4x. At this ratio, a dangerous mathematical certainty emerges. If we assume the average coupon on the debt is 3% (this is conservatively low), then the global economy needs to grow at a rate of 12% just to keep the tax base in line with the organically-growing debt balance (sovereign interest expense). Note: This does not include the increased deficits that are contemplated for battling the recessionary impacts of the COVID crisis.

In a debt/GDP spiral, the fiat currency becomes the error term, meaning that printing more fiat is the only solution that balances the growth in the numerator relative to the denominator. When more fiat is printed, the value of the outstanding fiat is debased. It is circular and error terms imply an impurity in the formula.

Therefore, when you lend a government money at time zero, you are highly likely to get your money back at time x; however, the value of that money will have been debased. That is a mathematical certainty. Assuming there is no contagion that leads to a default, the debt contract has been satisfied. But who is the fool? Moreover, with interest rates at historic lows, the contractual returns on the obligations will certainly not keep pace with the Consumer Price Index (CPI), let alone true inflation as measured by other less-manipulated baskets. And notice we have not even mentioned the return that would be required for a fair reward due to the credit risk.

I paraphrase the main question as follows: If countries can just print, they can never default, so why would CDS spreads widen? Make no mistake: sovereign credits do default even though they can print money.

Remember the Weimar hyperinflation following World War I, the Latin American Debt Crisis in 1988, Venezuela in 2020 and Turkey in 2021, where fiat is (actually or effectively) shoveled to the curb as garbage. There are plenty of other examples, just not in the “first world.” Regardless, it becomes a crisis of confidence and existing holders of government debt do not roll their obligations. Instead, they demand cash. Governments can “print” the cash, but if it is shoveled to the curb, we would all agree that it is a de facto default. Relying on economics professors/modern monetary theorists to opine that “deficits are a myth” is dangerous. The truth may be inconvenient, but that makes it no less true.

Conclusion

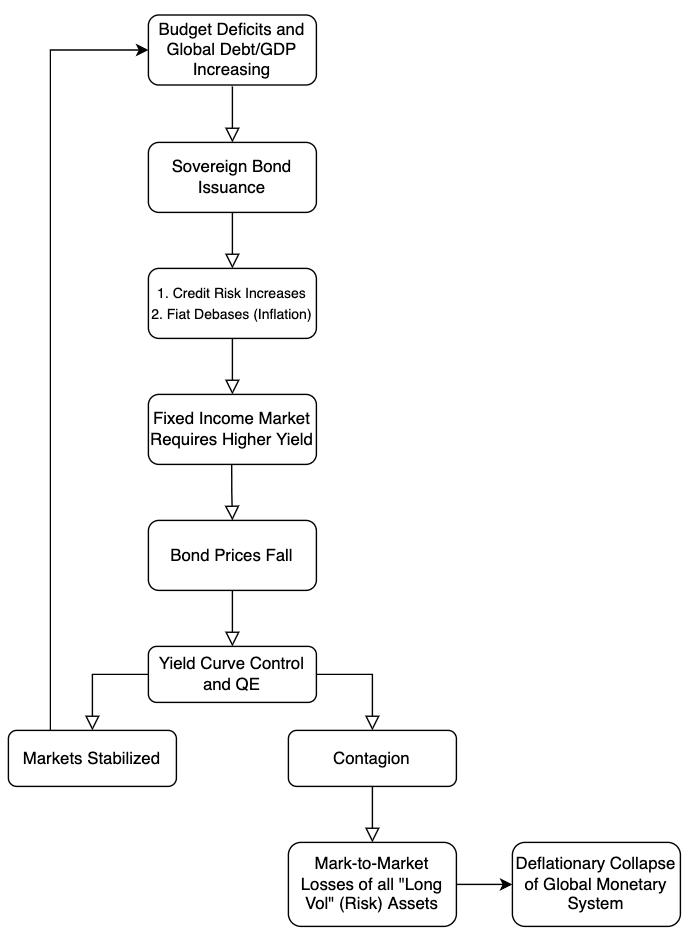

We conclude this section with a visual flowchart of how things could theoretically “fall apart.” Remember, systems work until they don’t. Slowly then suddenly…

A flow chart of how things fall apart.

Proceed accordingly. Risk happens fast.

This is a guest post by Greg Foss and Jason Sansone. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

ApeCoin (APE) continued its rebound relocation on March 24 as the company behind it raised hundreds of millions of dollars in a financing round led by Andreessen Horowitz.

APE's rate rose 7.5% intraday to reach around $14.50 per piece. Notably, the token's advantage relocation came as a part of a retracement rally that began at the start of this week when it was altering hands for as low as $9.50.

That pressed APE's week-to-date earnings up by 50%, making it one of the best-performing digital properties consideringthat March 21.

To wrap-up, ApeCoin digital currency came to presence on March 17, through an "airdrop" backed by Yuga Labs, the developer of the Bored Ape Yacht Club (BAYC), a collection of nonfungible tokens (NFTs) popular amongst celebs, sportspersons and endeavor capitalists, alike, for its so-called status sign.

Yuga Labs dropped 150 million APE — out of the overall 1 billion developed — amongst the owners of the Bored Ape NFTs, with each getting 10,904 tokens, worth over $158,000 as of March 24 for "free."

Meanwhile, owners of the rarest BAYC NFTs, the "Mutant Apes," got 2,042 APE, which expenses around $30,000 as of March 24's rate.

The company jobs APE as a governance and energy token to enable its holders to supervise and handle the so-called ApeCoin DAO, a decentralized self-governing company. As a result, holding an APE offers users the right to vote on choices proposed within the BAYC community.

"It will serve as a decentralized procedure layer for community-led efforts that drive culture forward into the metaverse," reads an excerpt from ApeCoin's authorities site.

The ApeCcoin neighborhood hasactually provided 5 propositions, consistingof the DAO structure; the ballot procedure; the allowance of the eco-friendly budgetplan; the guidelines for staking and the allotment of staking swimmingpool. More than half of the spendingplan goes to the videogame advancement. https://t.co/s1vq8v623g

Interestingly, Yuga Labs provided entities that assisted it launch APE, consistingof Andreessen Horowitz and Animoca Brands, about 14% of its overall supply, worth about $2 billion at March 24's rates. On March 22, the company raised $450 million from the verysame endeavor capitalists to worth at $4 billion.

Crypto exchange FTX likewise contributed to the financing round, which, as Yuga declared, will be utilized to broaden its advancement group and to supervise their coming joint endeavors, consistingof a metaverse job called "Otherside."

Nonetheless, changing to lower-timeframe charts programs APE trending up within a parallel rising channel with traders purchasing when the rate strikes the lower trendline and selling when it strikes the upper trendline.

As a result, APE's continuous rebound relocation might have it extend its benefit momentum towards the channel's upper trendline near $15, corresponding with another resistance level from March 18–19.

Meanwhile, APE has likewise been trying to recover $14.25 as its interim assistance. Failing to do so might threat an early pullback relocation towards the channel's lower trendline, likewise corresponding with its 20-hour rapid moving average (20-hour EMA; the green wave) near $13.50.

The views and viewpoints revealed here are entirely those of the author and do not always show the views of Cointelegraph.com. Every financialinvestment and trading relocation includes threat, you oughtto conduct your own researchstudy when making a choice.

Web3 is hailed as a innovation paradigm that is sustained by the developer economy and is in the future, or rather, the next advancement of the web. As we draw evolutionary contrasts of the innovation that underpinned whatever from details usage to material development, Web2 contributed an exceptional financial development and represented a substantial age in human advancement with brand-new methods to work, customer info and development in human civilization. So with this huge success of Web2, why is there a requirement for Web3?

As we reassess the web, which relies mainly on a coupleof central entities that have gadgets, channels of info that feeds the social media, mobile apps and supplies connection points inbetween service companies and applicants of these services, the control over these channels offers the custodian of this facilities not just monopolistic control however likewise a “too huge to stopworking” financial choke point. So reassessing the web, which was created mostly to relocation details and changed into moving worth and reality, is a basic shift in empowering developers and individuals and not simply the custodians on the facilities.

The chauffeurs that sustained this disruptive thinking were extreme evaluation and control of Web2 business, censorship enforcement by the existing control of info channels and the fast dissemination of info, which was a force for great as in understanding transfer however is now weaponized with the speed and accuracy of info and the dissemination of predisposition, skepticism and falseinformation — making it hard to determine inbetween signal and sound. These motorists suggest not just the dawn of a brand-new period however likewise the innovative nature of the human types to reassess, redesign and restore, shaping the next period of our development.

So how do we imagine this brand-new paradigm taking shape? As Web3 intends at thinking that the web takes another action to be self-dependent — leading to a entire brand-new set of innovation and procedure advancement, which will then be a structure of a creators-controlled economy that embarks on details and worth motion, and has discernable channels with integrated trust allowed by procedure. Blockchain and decentralization are typically promoted to be the allowing fundamental principles that are considered necessary to the advancement of such a platform. But priorto we beverage the decentralization Kool-Aid, I believe we ought to take a action back and reevaluate the success (and failures) of Web2 and more significantly, a shift to this brand-new paradigm, as I suspect the obstacles are not simply technology-driven.

To makeitpossiblefor a Web3-led developers’ economy that empowers developers and individuals, we requirement to veryfirst comprehend the imperatives of participatory economics, where the focus is mostly driven by self-governance, effectiveness, sustainability and the development of a decentralized financial system designed with strong rewards and safeguarded by procedures that require social ownership, self-managed works and responsibility for results.

Participatory economics stems from previous centuries of idea and experimentation around the concept that individuals must be able to handle their own lives with others (on the exactsame network airplane) cooperatively and relatively with guidelines ingrained in the reward economy that benefits involvement and punishes misbehavior and activities that the network views as unreasonable. In other words, for Web3 to work and provide on its assure, we requirement involvement.

At a extremely fundamental level, involvement, much like in the genuine world, can come through dedication of resources — such as systems, procedures, abilities, intellectual capital and knowledge andsoon, and worth produced must have an fair circulation amongst the different individuals based on the basic tenets of need and supply to address the fairness component. The financial worth produced would then requirement to be recognized, accounted for, shared and exchanged with other fungible and nonfungible properties to keep a balance in any financial network — all of this without any main accounting system or authority — to address the self-governance and procedure caused fair structure.

Web3, in its present context, starts to appearance like a stateful system of tokenized networks. Where these tokenized networks are not just drawingin capital, skill and innovation providing them a country–state (with their financial structure and in-network currencies) status however likewise are market locations and labs of co-creation inbetween different tasks. We haveactually started to see these manifest in numerous decentralized financing (DeFi) and nonfungible token (NFT) tasks, and in a real sense, they are producing metaversical synergies inbetween numerous tokenized networks.

To supply a real peer-to-peer, multi-token network (in a real sense, it’s metaverse) where tasks and people can co-create and bring their participative energy is basically the structure facilities required to provide the Web3 guarantee. While we haveactually seen unmatched development in the token-driven economy and rapid development in financialinvestment and evaluation of these jobs, I believe lotsof of these tasks neither embody the Web3 concepts of involvement nor have an financial output that adheres to Web3 tenets. The basic activeingredient doingnothave here is — involvement.

Evolution of Web3 economies and present volatility

Two essential innovation principles that permit us to determine inbetween information (for recognition and reality) and worth transfer (for the involvement economy) are the Semantic Web and decentralization, which will shape the future and helpwith the shift from the existing quickly growing Web2 to the morerecent ownership-driven Web3.

The Semantic Web extends the idea of file/information on the web to information that is of worth, helpingwith info that endsupbeing more significant (and important) when semantically connected with information. Data is then transformed to things of worth — leading to moneymaking and the responsibility aspects of Web3 concepts.

Decentralization, on the other hand, assistsin peer-to-peer networks such as blockchain and allows us to relocation tokenized worth — be they systemically produced (cryptocurrency) or caused (tokens that represent worth) — and address the independent and protocol-induced fairness aspects of Web3 concepts. At a really standard level, as we frame numerous synergistic environments emerging on Web3 concepts, it is reasonable to presume that their economies are interlinked. And as we construct a strong structure of Web3 with decentralized processing, affiliations and storage as fundamental structure obstructs, they looklike the Web2 cloud facilities however with a various financial structure and control points.

As jobs establish and develop, these tokenized worths would be inclusive of the cumulative worth of the underlying facilities, services and skill layers. This synergistic environment as manifested in the natural system will grow; and a effective community and economy will drawin skill, capital and resources with maintained shared interest.

For circumstances, a metaverse task that consistsof NFTs and liquid crypto properties for fungibility will likewise have as the source of its success decentralized storage for artifacts, curated information design and analytics for its operation, decentralized processing and so on, lifting all the services community that would makeup Web3 ecology.

Now, lotsof of these services are centralized so they that the difficulties of the present financial system are likewise intrinsic in them, significance they embark on on the pledge of Web3 however absence its concepts. This is rather apparent with the volatility of crypto and increased liquidity provisioning from standard financing in the kind of stablecoin or banking on-ramps that allow the complimentary circulation of liquidity from conventional financing, hence protecting not just the development however likewise the difficulties of the existing monetary system. So this linkage of volatility and stability of crypto markets is something we ought to goover and the effect of this on volatility and what it indicates for the parallel monetary systems of yield and returns.

For circumstances, a high yield in crypto markets will bringin liquidity, and while the risk-on risk-off formula at play will drawin capital and issuance of stablecoins, it likewise acquires the mechanics of worldwide macro, which indicates that any shifts in standard financing capital markets, interest rates, cash supply, inflation andsoon, which plays an crucial function in calculus that goes into possession assessment, start to effect the crypto market, which, in concept, is indicated to be independent and disruptive. What if we goal for self-sufficiency with really crypto liquid and fungible properties and let the financial system work and self-correct? I discover this formula worth the researchstudy and intriguing, however likewise paradoxical.

This shortarticle does not consistof financialinvestment suggestions or suggestions. Every financialinvestment and trading relocation includes danger, and readers oughtto conduct their own researchstudy when making a choice.

The views, ideas and viewpoints revealed here are the author’s alone and do not always show or represent the views and viewpoints of Cointelegraph.

Nitin Gaur is the creator and director of IBM Digital Asset Labs, where he develops market requirements and usage cases, and works towards making blockchain for the business a truth. He formerly served as chief innovation officer of IBM World Wire and of IBM Mobile Payments and Enterprise Mobile Solutions, and he established IBM Blockchain Labs, where he led the effort in developing the blockchain practice for the business. Gaur is likewise an IBM-distinguished engineer and an IBM master innovator with a abundant patent portfolio. Additionally, he serves as researchstudy and portfolio supervisor for Portal Asset Management, a multi-manager fund specializing in digital properties and DeFi financialinvestment methods.

Senator Warren and her group prepared a costs with objectives to heighten sanctions' impact on Russia, however ended up troubling much of the crypto market.

Cover art/illustration bymeansof CryptoSlate

Yesterday, a group of democratic co-sponsors led by Senator Warren introduced a expense entitled the Digital Asset Sanctions Compliance Enhancement Act. The costs provides specific preventativemeasures to appropriately avoid Russia from utilizing crypto to avert financial sanctions.

In addition to the truth that crypto can’t solitarily rescue Russia and that most nations are currently applying crypto sanctions, the presented safetymeasures use limitations on individuals who construct, run, and usage cryptocurrency networks even if they have no understanding or intent to aid anybody avert sanctions. Anyone who releases open-source softwareapplication or assistsin interaction amongst network individuals would fall under that meaning and face sanctions themselves.

What would takeplace if the expense passed?

The costs calls for sanctions on:

“Anyone who substantially and materially helped, sponsored, or offered monetary, product, or technological assistance for, or items or services to or in assistance of any [sanctioned] individual.”

This unclear meaning is really susceptible to be utilized in an overinclusive way. So let’s briefly go over the veryfirst stars that come to mind.

All exchange platforms

From the above sentence, exchange platforms are direct collocutors of “goods or services.” Even though non-compliant abroad crypto exchanges stay the most substantial risk versus Anti Money Laundering and Counter Financing of Terrorism, this act doesn’t target them just. As they are currently operating unlawfully, extra policies do really littlebit to modification their operations.

Moreover, the US Plocal can currently produce secondary sanctions on exchanges when essential. Therefore, this act will do absolutelynothing more than endanger all exchange platforms’ operations without offering strong benefit for measuring the criminaloffense.

All secret stars

In addition to the above declaration, the costs likewise enables:

“The Secretary of Treasury to execute a complete and indiscriminate restriction on exchanges or non-custodial deal facilitators doing company with anybody or any cryptocurrency address recognized to be, or might fairly be understood to be, associated with individuals in Russia.”

This declaration, together with the “persons offering product or technical assistance” definition from the above declaration might consistof actually everybody who is included in the crypto market.

An vast number of individuals contributed to the production of softwareapplication, which is utilized to either conduct company or sendout deals to approved people by 3rd celebrations. All designers who produced the code and all nodes, validators, miners, and all other comparable functions who aid the system work would be approved if this costs passes.

Innocent Russians

Based on these declarations, everybody who procedures deals after the approved activities would be guilty too, consideringthat their deals aid miners produce more obstructs and therefore combine the approval of the approved deal.

This likewise consistsof millions of Russian people, who have a greater possibility of being associated to the approved deals specified in the costs. These Russians might be versus the war and have no other alternative other than crypto to secure what’s left of their individual financialresources.

Commenting on the possible variety of the costs, the Founder of the Ukrainian crypto exchange, the Ukrainian federalgovernment Michael Chobanian stated that these Russians are the genuine opposition to Putin, and the last thing they requirement is more sanctions on themselves. He specified:

“Many civilians justifiably worry the seizure of retail deposits and desire to safeguard their capital. Purchasing digital possessions is an reliable indicates by which regular Russian residents can show their opposition to Putin’s routine by moving their costsavings out of the monetary system of the Russian ruble.”

Get your day-to-day wrap-up of Bitcoin, DeFi, NFT and Web3 news from CryptoSlate

Get an Edge on the Crypto Market 👇

Become a member of CryptoSlate Edge and gainaccessto our unique Discord neighborhood, more unique material and analysis.

Let’s take a closer look at today’s altcoins showing breakout signals. We’ll explain what the coin is, then dive into the trading charts and provide some analysis to help you decide.

1. Chainlink (LINK)

The Chainlink Network LINK is driven by a large open-source community of data providers, node operators, smart contract developers, researchers, security auditors, and more. The company focuses on ensuring that decentralised participation is guaranteed for all node operators and users looking to contribute to the network. Chainlink allows blockchains to securely interact with external data feeds, events and payment methods, providing the critical off-chain information needed by complex smart contracts to become the dominant form of digital agreement.

LINK Price Analysis

At the time of writing, LINK is ranked the 24th cryptocurrency globally and the current price is US$12.50. Let’s take a look at the chart below for price analysis:

LINK‘s early January spike retraced near $12.46 into the consolidation that began the impulse before bouncing to $14.30.

This consolidation could provide support again, although bears would first have to push the price through possible support near $12.00. The market’s structure may be shifting bearish, with $13.52 likely to provide some resistance if this is the case. A sustained bearish move could reach the swing low near $11.63 before finding support near $10.71.

However, the bullish higher-timeframe trend might prevail, with relatively equal highs near $16.78 potentially giving an attractive target to lure the price over the monthly open. If so, the price could reach for the midpoint of the December wick near $20.58.

2. Dydx (DYDX)

DYDX is a governance token that allows the dYdX community to truly govern the dYdX Layer 2 Protocol. By enabling shared control of the protocol, DYDX allows traders, liquidity providers and partners of dYdX to work collectively towards an enhanced protocol. DYDX enables a robust ecosystem around governance, rewards and staking, each designed to drive future growth and decentralisation of dYdX, resulting in a better experience for users.

DYDX Price Analysis

At the time of writing, DYDX is ranked the 140th cryptocurrency globally and the current price is US$4.83. Let’s take a look at the chart below for price analysis:

DYDX consolidates between $4.60 and $5.90 with the bulk of the volume concentrated in the lower half of the range. The price does not indicate a clear longer-term direction yet as stop orders build on both sides of the range.

Range traders will likely take profits or sell near $5.32. A stop run and swift rejection above $5.74 could provide a more favourable risk-to-reward entry for bears. An old 4h gap around $6.35 might cap this stop run.

Bulls will likely accumulate more long positions on a run below the relatively equal lows near $4.70. Little exists below the current range to identify precise support levels. However, the area between $4.58 and $4.50 could also give support during a deeper stop run.

If the price does break out decisively to the upside, the swing high at $6.15 provides a reasonable target. The highs and daily resistance levels between $6.47 and $6.80 may provide a second target.

3. Internet Computer (ICP)

The Internet Computer ICP is the world’s first blockchain that runs at web speed with unbounded capacity. It also represents the third major blockchain innovation, alongside Bitcoin and Ethereum – a blockchain computer that scales smart contract computation and data, runs them at web speed, processes and stores data efficiently, and provides powerful software frameworks to developers. By making this possible, the Internet Computer enables the complete reimagination of software, providing a revolutionary new way to build tokenised internet services, pan-industry platforms, decentralised financial systems, and even traditional enterprise systems and websites.

ICP Price Analysis

At the time of writing, ICP is ranked the 36th cryptocurrency globally and the current price is US$15.64. Let’s take a look at the chart below for price analysis:

During January, ICP also turned the corner, breaking a key swing high. This move could suggest a longer-term bullish trend.

The swing high near $26.24 stands out as a bullish target and marks an area of probable resistance. Further continuation could reach into possible resistance starting near $31.35.

Even if the bearish trend continues, a stop run at the recent swing low near $15.00 into possible support beginning near $14.67 is reasonable. If the price reaches further down, the swing low and possible support near $13.97 might provide another downside target.

The area near $13.25 could also provide support. However, a drop this far could suggest a stop run below the higher-timeframe relatively equal lows near $12.80 into possible support beginning around $12.00.

These coins have high liquidity on Binance Exchange, so that could help with trading on AUD/USDT/BTC pairs. And if you’re looking at buying and HODLing cryptos, then Swyftx Exchange is an easy-to-use popular choice in Australia.

Disclaimer:

The content and views expressed in the articles are those of the original authors own and are not necessarily the views of Crypto News. We do actively check all our content for accuracy to help protect our readers. This article content and links to external third-parties is included for information and entertainment purposes. It is not financial advice. Please do your own research before participating.

Cryptocurrencies

Cryptocurrencies