This is a viewpoint editorial by Taimur Ahmad, a college student at Stanford University, concentrating on energy, ecological policy and global politics.

This is a viewpoint editorial by Taimur Ahmad, a college student at Stanford University, concentrating on energy, ecological policy and global politics.Author's note: This is the very first part of a three-part publication.

Part 1 presents the Bitcoin requirement and examines Bitcoin as an inflation hedge, going deeper into the idea of inflation.

Part 2 concentrates on the present fiat system, how cash is developed, what the cash supply is and starts to talk about bitcoin as cash.

Part 3 looks into the history of cash, its relationship to state and society, inflation in the Global South, the progressive case for/against Bitcoin as cash and alternative use-cases.

Bitcoin As Money: Progressivism, Neoclassical Economics, And Alternatives Part I

Prologue

I as soon as heard a story that set me on my journey to attempt and comprehend cash. It goes something like:

Imagine a traveler pertains to a little, rural town and remains at the regional inn. Similar to any decent location, they are needed to pay 100 diamonds (that's what the town utilizes as cash) as a damage deposit. The next day, the inn owner recognizes that the traveler has quickly left town, leaving the 100 diamonds. Considered that it is not likely the traveler will venture back, the owner is thrilled at this turn of occasions: a 100 diamond perk! The owner heads to the regional baker and settles their financial obligation with this money; the baker then goes off and settles their financial obligation with the regional mechanic; the mechanic then settles the tailor; and the tailor then settles their financial obligation at the regional inn!

This isn't the delighted ending. The next week, the exact same traveler returns to get some baggage that had actually been left. The inn owner, now feeling bad for still having the deposit and freed from settling their financial obligation to the baker, chooses to advise the traveler of the 100 diamonds and hand them back. The traveler nonchalantly accepts them and remarks "oh these were simply glass anyways," prior to squashing them under his feet.

A stealthily easy story, however constantly difficult to cover my head around it. There are numerous concerns that show up: if everybody in the town owed money to each other, why could not they simply cancel it out (coordination issue)? Why were the townsfolk spending for services to each other in financial obligation-- IOUs-- however the traveler was needed to pay cash (trust issue)? Why did nobody check whether the diamonds were genuine, and could they have even if they desired (standardization/quality issue)? Does it matter that the diamonds weren't genuine (what actually is cash then)?

Introduction

We remain in the middle of a poly-crisis, to obtain from Adam Tooze. As cliché as it sounds, modern-day society is a significant inflection point throughout numerous, interconnected fronts. Whether it is the international financial system-- the U.S. and China playing complementary functions as customer and manufacturer respectively-- the geopolitical order-- globalization in a unipolar world-- and the eco-friendly environment-- low-cost nonrenewable fuel source energy fueling mass intake-- the structures atop which the previous couple of years were developed are completely moving.

The advantages of this mostly steady system, although unequal and at fantastic expense to lots of social groups, such as low inflation, worldwide supply chains, a form of trust, and so on, are rapidly unraveling. This is the time to ask huge, essential concerns, the majority of which we have actually been too scared or too sidetracked to request for a long period of time.

The concept of cash is at the heart of this. Here I do not indicate wealth always, which is the topic of numerous conversations in modern-day society, however rather the principle of cash. Our focus is normally on who has just how much cash (wealth), how we can get more of it for ourselves, asking is the present circulation fair, and so on. Beneath this discourse is the presumption that cash is a mostly inert thing, practically a sacrilegious things, that gets walked around every day.

In the previous couple of years, nevertheless, as financial obligation and inflation have ended up being more prevalent subjects in mainstream discourse, concerns around cash as an idea have gathered increasing attention:

- What is cash?

- Where does it originate from?

- Who manages it?

- Why is something cash however the other isn't?

- Does/can it alter?

Two concepts and theories that have actually controlled this discussion, for much better or for even worse, are Modern Monetary Theory (MMT) and alternative currencies (mainly Bitcoin). In this piece, I will be mainly concentrating on the latter and seriously examining the arguments underpinning the Bitcoin requirement-- the theory that we must change fiat currency with Bitcoin-- its possible risks, and what alternative functions Bitcoin might have. This will likewise be a review of neoclassical economics which governs mainstream discourse outside the Bitcoin neighborhood however likewise forms the structure for numerous arguments on top of which the Bitcoin basic rests.

Why Bitcoin? When I got exposed to the crypto neighborhood, the mantra I encountered was "crypto, not blockchain." While there are benefits to that, for the particular use-case of cash specifically, the mantra to concentrate on is "Bitcoin, not crypto." This is a crucial point since analysts outside the neighborhood frequently conflate Bitcoin with other crypto possessions as part of their reviews. Bitcoin is the just genuinely decentralized cryptocurrency, without a pre-mine, and with set guidelines. While there are lots of speculative and doubtful jobs in the digital possession area, just like other possession classes, Bitcoin has actually well developed itself to be a really ingenious innovation. The proof-of-work mining system, that frequently comes under attack for energy usage (I composed versus that and described how BTC mining assists tidy energy here), is important to Bitcoin differing from other crypto possessions.

To duplicate for the sake of clearness, I will be simply concentrating on Bitcoin just, particularly as a financial possession, and primarily evaluating arguments originating from the "progressive" wing of Bitcoiners. For the majority of this piece, I will be describing the financial system in Western nations, concentrating on the Global South at the end.

Since this will be a long, sometimes meandering, set of essays, let me offer a fast summary of my views. Bitcoin as cash does not work since it is not an exogenous entity that can be programmatically repaired. Designating moralistic virtues to cash (e.g. noise, reasonable, and so on) represents a misconception of cash. My argument is that cash is a social phenomenon, coming out of, and in some methods representing, socioeconomic relations, class structure, and so on. The product truth of the world produces the financial system, not vice versa. This has actually constantly held true. Cash is an idea continuously in flux, always so, and need to be flexible to soak up the complex motions in an economy, and need to be versatile to change to the distinctive characteristics of each society. Cash can not be separated from the political and legal organizations that produce residential or commercial property rights, the market, and so on. If we wish to alter the damaged financial system these days-- and I concur it is broken-- we need to concentrate on the ideological structure and organizations that form society so we can much better utilize existing tools for much better ends.

Disclaimer: I hold bitcoin.

Critique Of The Current Monetary System

Proponents of the Bitcoin requirement make the following argument:

Government control of the cash supply has actually resulted in widespread inequality and decline of the currency. The Cantillon impact is among the primary motorists behind this growing inequality and financial distortion. The Cantillon impact being a boost of cash supply by the state prefers those who are close to the centers of power due to the fact that they get access to it.

This absence of responsibility and openness of the financial system has causal sequences throughout the socioeconomic system, consisting of reducing buying power and restricting the conserving abilities of the masses. A programmatic financial property that has actually repaired guidelines of issuance, low barriers to entry and no governing authority is needed to counter the prevalent results of this corrupt financial system which has actually produced a weak currency.

Before I start to examine these arguments, it is necessary to locate this motion in the bigger socioeconomic and political structure we reside in. For the past 50- odd years, there is significant empirical proof to reveal that genuine salaries have actually been stagnant even when efficiency has actually been increasing, inequality has actually been rising greater, the economy has actually been progressively financialized which has actually benefited the rich and property owners, monetary entities have actually been associated with corrupt and criminal activities and the majority of the Global South has actually experienced financial chaos-- high inflation, defaults, and so on,-- under an exploitative international monetary system. The neoliberal system has actually been unequal, overbearing and duplicitous.

During the exact same duration, political structures have actually been failing, with even democratic nations having fallen victim to state capture by the elite, leaving little area for political modification and responsibility. While there are numerous rich advocates of Bitcoin, a considerable percentage of those arguing for this brand-new requirement can be seen as those who have actually been "left behind" and/or acknowledge the grotesqueness of the existing system and are merely looking for a method out.

It is necessary to comprehend this as a description to why there is an increasing variety of "progressives"-- loosely specified as individuals arguing for some kind of equality and justice-- who are ending up being pro-Bitcoin requirement. For years, the concern of "what is cash?" or the fairness of our monetary system has actually been fairly missing from mainstream discourse, buried under Econ-101 misconceptions, and restricted to primarily ideological echo chambers. Now, as the pendulum of history reverses towards populism, these concerns have actually ended up being mainstream once again, however there is a scarcity of those in the specialist class that can adequately be considerate towards, and coherently react to, individuals's issues.

Therefore, it is crucial to comprehend where this Bitcoin basic story emerges from and to not outrightly dismiss it, even if one disagrees with it; rather, we should acknowledge that a number of us doubtful of the present system share a lot more than we disagree upon, a minimum of at a very first concepts level, which taking part in dispute beyond the surface area level is the only method to raise cumulative conscience to a phase that makes modification possible.

Is A Bitcoin Standard The Answer?

I will try to tackle this concern at numerous levels, varying from the more functional ones such as Bitcoin being an inflation hedge, to the more conceptual ones such as the separation of cash and The State.

Bitcoin As An Inflation Hedge

This is an argument that is extensively utilized in the neighborhood and covers a variety of functions crucial to Bitcoiners (e.g., defense versus loss of acquiring power, currency decline). Up till in 2015, the basic claim was that as rates are constantly increasing under our inflationary financial system, Bitcoin is a hedge versus inflation as its cost increases (by orders of magnitude) mo re than the cost of items and services. This constantly appeared like an odd claim due to the fact that throughout this duration, numerous threat properties carried out incredibly well, and yet they are not considered as inflation hedges in any method. And likewise, established economies were running under a nonreligious low inflation routine so this claim was never ever truly checked.

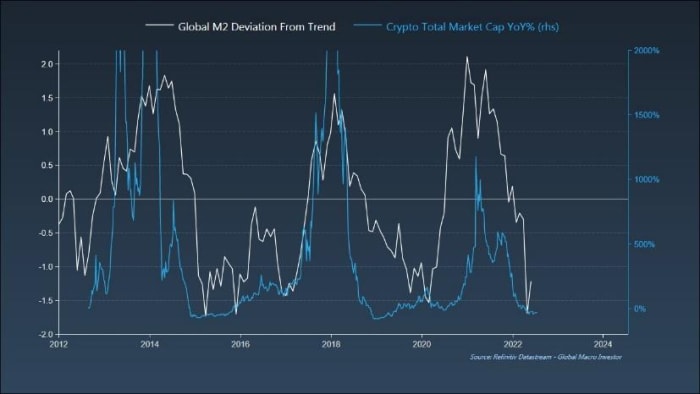

More significantly however, as costs rose greater over the previous year and Bitcoin's cost plunged, the argument moved to "Bitcoin is a hedge versus financial inflation," implying that it does not hedge versus an increase in the rate of products and services per se, however versus the "decline of currency through cash printing." The chart below is utilized as proof for this claim.

Source: Raoul Pal's Twitter

This is likewise a strange argument for numerous factors, each of which I will describe in more information:

- It once again depends on the claim that Bitcoin is distinctively a "hedge" and not merely a risk-on property, comparable to other high-beta properties that have actually carried out well over durations of increasing liquidity.

- It depends on the monetarist theory that increase in the cash supply straight and imminently causes a boost in costs (if not, then why do we appreciate the cash supply to start with).

- It represents a misconception of M2, cash printing, and where cash originates from.

1. Is Bitcoin Simply A Risk-On Asset?

On the very first point, Steven Lubka on a current episode of the What Bitcoin Did podcast said that Bitcoin was a hedge versus inflation triggered through extreme financial growth and not when that inflation was supply-side, which, as he appropriately mentioned, is the present scenario. In a current piece on the very same subject, he reacts to the review that other risk-on properties likewise increase throughout durations of financial growth by composing that Bitcoin increases more than other properties which just Bitcoin need to be thought about as a hedge due to the fact that it is "simply cash," while other possessions are not.

However, the degree to which a possession's cost increases should not matter as a hedge as long as it is favorably associated to the rate of items and services; I 'd even argue that cost increasing excessive-- undoubtedly subjective here-- presses a possession from a hedge to speculative. And sure, his point that possessions like stocks have distinctive dangers like bad management choices and financial obligation loads that make them clearly various to Bitcoin holds true, however other elements such as "danger of obsolescence," and "other real-world difficulties," to estimate him straight, use to Bitcoin as much as they use to Apple stock.

There are numerous other charts that reveal Bitcoin has a strong connection with tech stocks in specific, and the equity market more broadly. The reality is that the supreme driving aspect behind its cost action is the modification in international liquidity, especially U.S. liquidity, since that is what chooses how far throughout the threat curve financiers want to press out. In times of crisis, such as now, when safe house properties like the USD are having a strong run, Bitcoin is not playing a comparable function.

Therefore, there does not appear to be any analytical factor that Bitcoin trades in a different way to a risk-on possession riding liquidity waves, which it ought to be dealt with, just from a financial investment perspective, as anything various. Given, this relationship might alter in the future however that's for the marketplace to choose.

2. How Do We Define Inflation And Is It A Monetary Phenomenon?

It is vital to the Bitcoiner argument that increases in cash supply results in currency decline, i.e., you can purchase less products and services due to greater rates. This is difficult to even focus as an argument since the meaning of inflation appears to be in flux. For some, it is merely a boost in the rate of items and services (CPI)-- this appears like an user-friendly principle since that's what individuals as customers are most exposed to and appreciate. The other meaning is that inflation is a boost in the cash supply-- real inflation as some refer to it as-- despite the influence on the rate of products and services, despite the fact that this must cause rate boosts ultimately This is summed up by Milton Friedman's, now meme-ified in my viewpoint, quote:

" Inflation is constantly and all over a financial phenomenon in the sense that it is and can be produced just by a more quick boost in the amount of cash than in output."

Okay so let's attempt to comprehend this. Rate boosts due to non-monetary causes, such as supply chain problems, are not inflation. Cost boosts due to a growth of the cash supply are inflation. This lags Steve Lubka's point, a minimum of how I comprehended it, about Bitcoin being a hedge versus real inflation however not the existing bout of supply-chain caused high costs. (Note: I am utilizing his work particularly due to the fact that it was well articulated however lots of others in the area make a comparable claim).

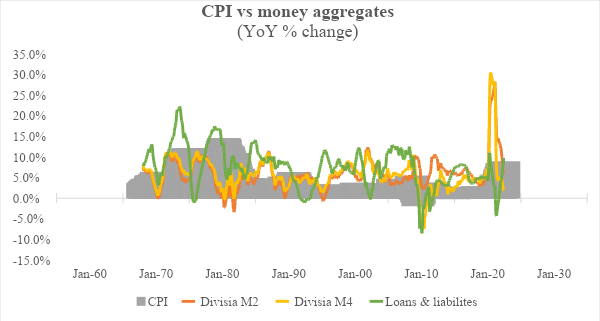

Since nobody is arguing the impact of supply chain and other physical restraints on rates, let's concentrate on the 2nd declaration. Why does modification in the cash supply even matter unless it is connected to a modification in costs, regardless of when those rate modifications happen and how uneven they are? Here is a chart revealing yearly portion modification in various steps of the cash supply and CPI.

Data source: St. Louis Fed; Center for Financial Stability

Technical note: M2 is a narrower procedure of cash supply than M4 as the previous does not consist of extremely liquid cash alternatives. The Federal Reserve in the U.S. just supplies M2 information as the broadest step of cash supply due to the fact that of the opaqueness of the monetary system which restricts appropriate evaluation of the broad cash supply. Here I utilize the Divisia M2 since it uses a methodologically remarkable estimate (by using weight to various types of cash) rather than the Federal Reserve's technique which is a simple-sum average (regardless, the Fed's M2 information is carefully lined up with Divisia's). Loans and leases is a procedure of bank credit, and as banks produce cash when they provide rather than recycling cost savings, as I discuss later on, this is essential to include.

We can see from the chart that there is weak connection in between modifications in cash supply and CPI. From the mid-1990 s till the early 2000 s, the rate of modification of cash supply is increasing while inflation is trending lower. The reverse holds true in the early 2000 s when inflation was getting however cash supply was boiling down. Post-2008 possibly stands apart the most since it was the start of the quantitative alleviating routine when reserve bank balance sheets grew at extraordinary rates and yet established economies constantly stopped working to fulfill their own inflation targets.

One prospective counterargument to this is that inflation can be discovered in property and stocks, which have actually been rising greater through the majority of this duration. While there is a certainly strong connection in between these property costs and M2, I do not believe stock exchange gratitude is inflation since it does not affect the acquiring power of customers and for this reason, does not need a hedge. Exist distributional concerns that cause inequality? Definitely. For now I desire to focus on the inflation narratively entirely. With concerns to real estate rates, it's challenging to count that as inflation since realty is a significant financial investment lorry (which is a deep structural issue in and of itself).

Therefore, empirically there is no considerable proof that a boost in M2 always results in a boost in CPI (it deserves advising here that I am concentrating on established economies mostly and will attend to the subject of inflation in the Global South later on). If there was, Japan would not be stuck in a low inflationary economy, well listed below its inflation target, in spite of the growth of the Bank of Japan balance sheet over the previous couple of years. The existing inflationary bout is since of energy costs and supply chain interruptions, which is why nations in Europe-- with their high reliance on Russian gas and improperly thought-out energy policy-- for instance, are dealing with greater inflation than other industrialized nations.

Sidenote: it was fascinating to see Peter McCormack's response when Jeff Snider made a comparable case (concerning M2 and inflation) on the What Bitcoin Did podcast Peter said how this made good sense however felt so counter to the dominating story.

Even if we take the monetarist theory as proper, let's enter some specifics. The essential formula is MV=PQ.

M: cash supply.

V: speed of cash.

P: rates.

Q: amount of products and services.

What these M2 based charts and analyses miss out on is how the speed of cash modifications. Take2020 The M2 cash supply rose greater due to the fact that of the financial and financial reaction of the federal government, leading numerous to anticipate devaluation around the corner. While M2 increased in 2020 by ~25%, the speed of cash reduced by ~18%. Even taking the monetarist theory at face worth, the characteristics are more complex than just drawing a causal link in between cash supply boost and inflation.

As for those who will raise the Webster dictionary meaning of inflation from the early 20 th century as a boost in cash supply, I 'd state that modification in cash supply under the gold requirement suggested something totally various to what it is today (dealt with next). Friedman's claim, which is a core part of the Bitcoiner argument, is basically a truism. Yes, by meaning greater rates, when not due to physical restrictions, is when more cash is chasing after the exact same items. That does not in and of itself equate to the reality that boost in the cash supply demands a boost in costs since that extra liquidity can open extra capability, lead to efficiency gains, broaden the usage of deflationary innovations, and so on. This is a main argument for (trigger caution here) MMT, which argues that targeted usage of financial costs can broaden capability, especially through targeting the "reserve army of the out of work," as Marx called it, and using them instead of treating them as sacrificial lambs at the neoclassical altar.

To bring this indicate a close then, it's difficult to comprehend how inflation is, for all intents and functions, anything various to a boost in CPI. And if the financial growth causes inflation mantra does not hold, then what is the benefit behind Bitcoin being a "hedge" versus that growth? Exactly what is the hedge versus?

I will confess there are a wide variety of concerns with how CPI is determined, however it is indisputable that modifications in rates occur due to the fact that of a myriad of factors throughout the demand-side and supply-side spectrum. This reality has actually likewise been kept in mind by Powell, Yellen, Greenspan, and other main lenders (ultimately), while numerous heterodox financial experts have actually been arguing this for years. Inflation is an incredibly complex principle that can not be just lowered to financial growth. This calls into concern whether Bitcoin is a hedge versus inflation if it is not safeguarding worth when CPI is rising, and that this principle of hedging versus financial growth is simply chicanery.

In Part 2, I describe the existing fiat system, how cash gets produced (it's not all the federal government's doing), and what Bitcoin as cash might do not have.

This is a visitor post by Taimur Ahmad. Viewpoints revealed are totally their own and do not always show those of BTC, Inc. or Bitcoin Magazine.

Read More https://bitcofun.com/is-bitcoin-an-inflation-hedge-a-critique-of-the-bitcoin-as-money-narrative/?feed_id=36467&_unique_id=631b2ef87a585

No comments:

Post a Comment